This reflects the salary and CETV pension funds of Executive board members only.

A more detailed insight of each board member will be available soon.

What is a Pension Cash Equivalent Transfer Value/ Cash Equivalent Benefit statement?

A CETV or CEB statement reflects the capital value of the pension benefits (i.e income and/or potential lump sum) that have been accrued to date, or which are in payment.

With a money purchase scheme, the CETV is purely the transfer value of the funds that have accrued to date. The transfer value may be different to the actual fund values, depending on scheme penalties.

The CETV of final salary schemes rarely reflects the true value of the accumulated pension rights. If the scheme is short of money, the transfer value may be reduced to reflect the underfunding position. This is a complex area and proper financial advice should be sought.

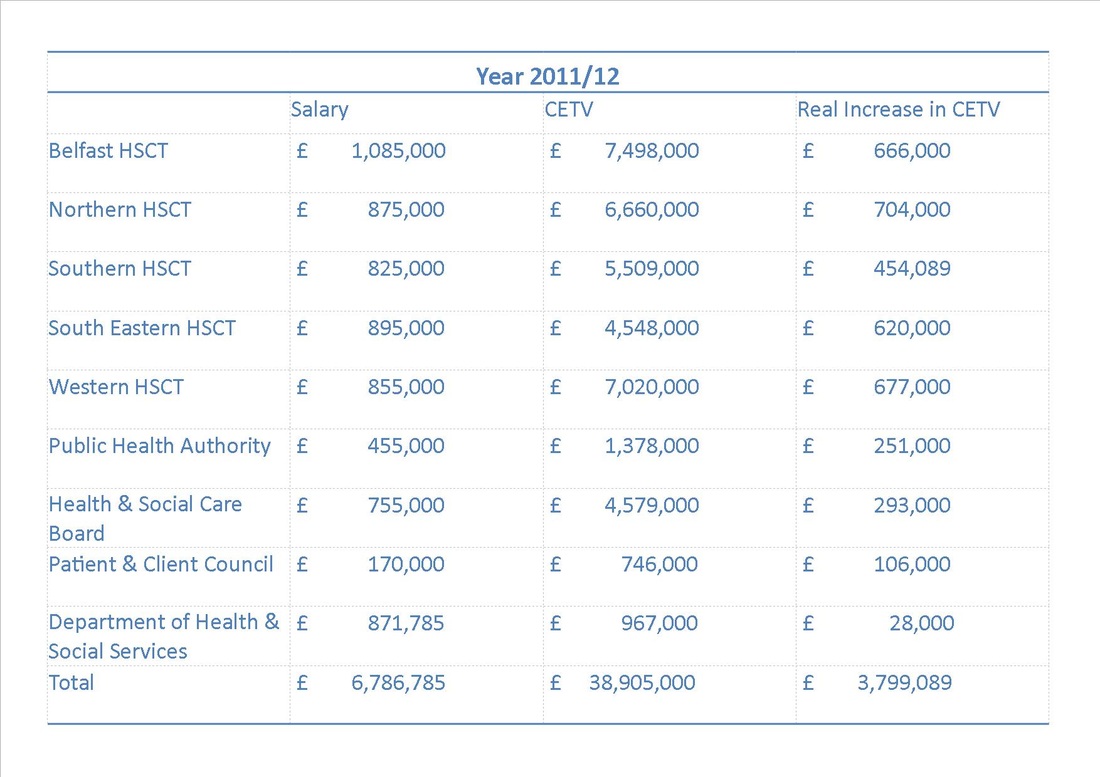

14. Cash Equivalent Transfer Values

A Cash Equivalent Transfer Value (CETV) is the actuarially assessed capitalised value of the pension scheme benefits accrued by a member at a particular point in time. The benefits valued are the member’s accrued benefits and any contingent spouse’s pension payable from the scheme. A CETV is a payment made by a pension scheme or arrangement to secure pension benefits in another pension scheme or arrangement when the member leaves a scheme and chooses to transfer the benefits accrued in their former scheme. The pension figures shown relate to the benefits that the individual has accrued as a consequence of their total membership of the pension scheme, not just their service in a senior capacity to which disclosure applies. The CETV figures, and from 2003-04 the other pension details, include the value of any pension benefit in another scheme or arrangement which the individual has transferred to the CSP arrangements. They also include any additional pension benefit accrued to the member as a result of their purchasing additional years of pension service in the scheme at their own cost. CETVs are calculated in accordance with The Occupational Pension Schemes (Transfer Values) (Amendment) Regulations and do not take account of any actual or potential benefits resulting from Lifetime Allowance Tax which may be due when pension benefits are taken.

The actuarial factors that are used in the CETV calculation were changed during 2011, due to changes in demographic assumptions. This means that the CETV in this year’s report for 31 March 2011 will not be the same as corresponding figure shown in last year’s report.

15. Real increase in CETV

This reflects the increase in CETV effectively funded by the employer. It does not include the increase in accrued pension due to inflation, contributions paid by the employee (including the value of any benefits transferred from another pension scheme or arrangement) and uses common market valuation factors for the start and end of the period.

What is a Pension Cash Equivalent Transfer Value/ Cash Equivalent Benefit statement?

A CETV or CEB statement reflects the capital value of the pension benefits (i.e income and/or potential lump sum) that have been accrued to date, or which are in payment.

With a money purchase scheme, the CETV is purely the transfer value of the funds that have accrued to date. The transfer value may be different to the actual fund values, depending on scheme penalties.

The CETV of final salary schemes rarely reflects the true value of the accumulated pension rights. If the scheme is short of money, the transfer value may be reduced to reflect the underfunding position. This is a complex area and proper financial advice should be sought.

14. Cash Equivalent Transfer Values

A Cash Equivalent Transfer Value (CETV) is the actuarially assessed capitalised value of the pension scheme benefits accrued by a member at a particular point in time. The benefits valued are the member’s accrued benefits and any contingent spouse’s pension payable from the scheme. A CETV is a payment made by a pension scheme or arrangement to secure pension benefits in another pension scheme or arrangement when the member leaves a scheme and chooses to transfer the benefits accrued in their former scheme. The pension figures shown relate to the benefits that the individual has accrued as a consequence of their total membership of the pension scheme, not just their service in a senior capacity to which disclosure applies. The CETV figures, and from 2003-04 the other pension details, include the value of any pension benefit in another scheme or arrangement which the individual has transferred to the CSP arrangements. They also include any additional pension benefit accrued to the member as a result of their purchasing additional years of pension service in the scheme at their own cost. CETVs are calculated in accordance with The Occupational Pension Schemes (Transfer Values) (Amendment) Regulations and do not take account of any actual or potential benefits resulting from Lifetime Allowance Tax which may be due when pension benefits are taken.

The actuarial factors that are used in the CETV calculation were changed during 2011, due to changes in demographic assumptions. This means that the CETV in this year’s report for 31 March 2011 will not be the same as corresponding figure shown in last year’s report.

15. Real increase in CETV

This reflects the increase in CETV effectively funded by the employer. It does not include the increase in accrued pension due to inflation, contributions paid by the employee (including the value of any benefits transferred from another pension scheme or arrangement) and uses common market valuation factors for the start and end of the period.

RSS Feed

RSS Feed